Part I: Introduction to Personal Finance

If you haven’t read those sections yet, I highly recommend you do so.

Coming Full Circle

Now that you’ve got your categories set up and you’ve begun tracking your expenses, you can start to put together a budget. This is where it all comes full circle and you can actually start to see things come to life and turn feedback into results.

Although different applications approach the budgeting process differently in how you set it up or track it, there are some basic principles that are universal that I recommend. It’s a good idea to set up two budgets to track income and expenses for the two most common periods in which trends occur.

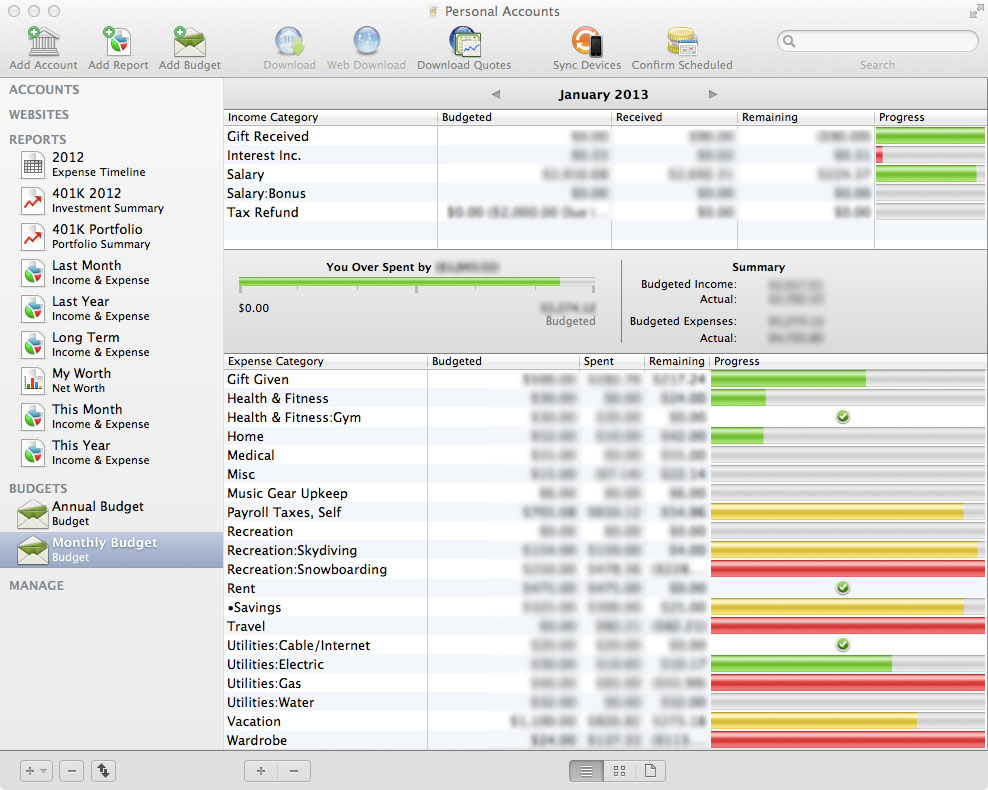

Monthly Budget

Since most of your fixed expenses will occur on a monthly basis (rent/mortgage, utilities, phone bill, etc.) you should first set up a monthly budget to keep track of what’s happening during that month. It’s good to review at the beginning of each month, and make projections based on the expenses you expect that month.

The monthly budget should come together relatively quickly, as you’ll see in a good 2-3 months what your spending trends tend to look like. The monthly budget becomes extremely useful for setting your short term goals, planning for upcoming bills and understanding what you need to do to maintain a positive cash flow.

Monthly Budget

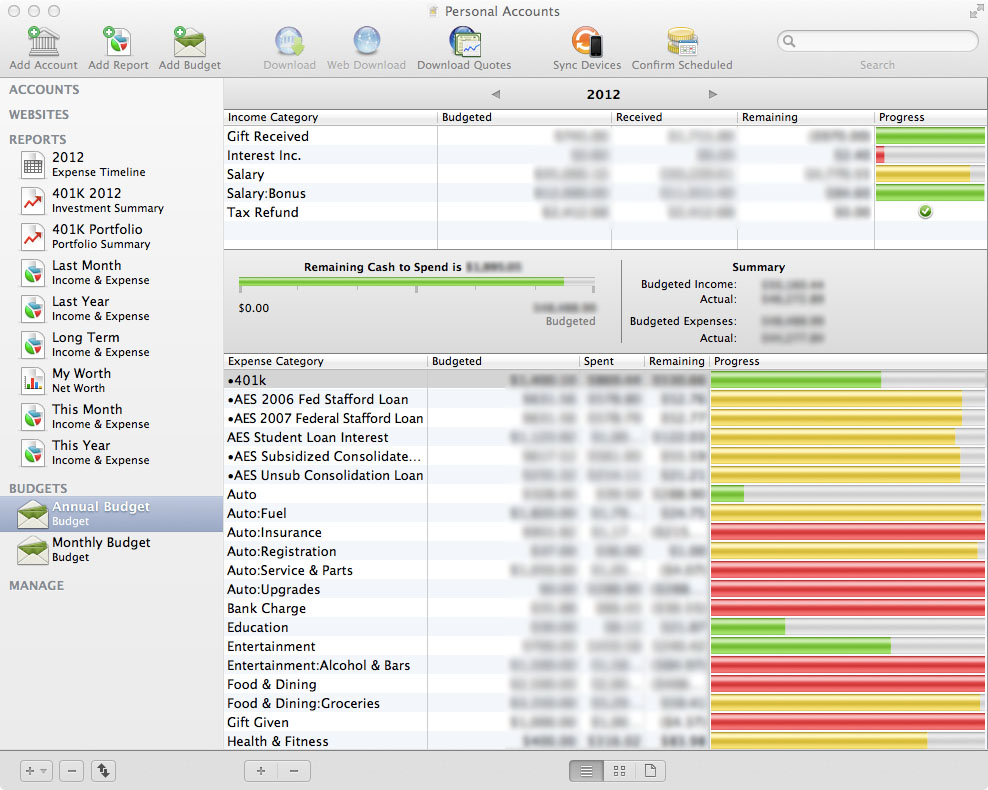

Annual Budget

The annual budget is your big picture budget, and allows you to keep track of more irregular expenses as well as income. The annual budget is important if your earnings have seasonal fluctuations, and it’s also very useful to plan ahead for those once-a-year expenses. Creating an annual budget will help you set goals for savings, and keep you aware of big expenses that seem to come out of nowhere (but really you just forgot about them).

The first year will be a guessing game. Once you have your monthly budget updated for 2-3 months, you can start to come up with averages and estimate what you’ll spend in each category that year, although it will be just that, an estimate. But after 1-2 years of tracking expenses and creating annual budgets, you will be able to create a VERY clear plan for the year. This is instrumental to me for setting financial goals for the longer term.

Annual Budget

Review Your Budget Often

The beginning of each year is a great time to assess your budget and reevaluate goals. I like to take the first week in January to really dig deep and look at past trends and future projections. I’d also recommend reviewing your budget once a week, but at least twice a month. Personal finance applications give you a great visual representation of your progress which really shows you how you’re doing.

Budgeting Tips

- Set an electronic calendar reminder recurring on the first of each month labeled “Close and Review Budget”. This will get you in the habit of checking how well you did last month, and remind you to review, consider and/or alter your budget for the upcoming month.

- During my monthly review, I like to print out the current month from my calendar, then mark down my upcoming expenses and bills, their due dates, and when I want them to be withdrawn in relation to my pay periods. I can then schedule the transactions ahead of time and make sure the money will be in my checking account.

- Budget your savings as an expense, that way you make sure you’re not counting it as money you have to spend.

- Always allow room for error and unforeseen expenses. Budget for less expenses than income (even after budgeting your savings as an expense). This will help to build a little cushion of savings and unforeseen expenses into your budget.

- Set concrete goals and work towards them. For example, set a goal for a percentage of your income that you want to save. Once you actually have it in numbers, and shown in your budget, you will easily be able to see what other categories need to change to acheive those goals.

- When setting budget goals, you are often times effectively changing your habits. For this reason, it is usually best to make small incrimental changes. For example, cutting 10% off your dining out expense might require eating less, cooking more, eating at cheaper restaurants and/or finding better deals. Either way, you’re doing something different, so it may require some adjustment. Adjust your goals as you get better at meeting them.

The Bottom Line

Budgeting is really quite simple when you categorize your expenses properly. It doesn’t take much time, and the automated nature of the applications I’ve covered in Part I really takes most of the work out of it as well. All you really have to do is pay attention to upcoming bills and expenses.

Taking these steps to track your expenses will make you more aware of the decisions you are making with your money, and will ultimately lead you to becoming better at managing it and planning ahead, which is a requirement for buidling wealth and cruising into retirement.

Do you have any tips for money management? Any software suggestions that I left out, or just questions on anything? If so, leave a comment below, I’d love to hear it!

Thanks for reading, and remember – RUN YOUR LIFE LIKE A BUSINESS!